HD Korea Shipbuilding Just Hit $2.7 Billion in Operating Profit — Here’s the Full Picture

In 2022, HD Korea Shipbuilding & Offshore Engineering (HD KSOE) posted an operating loss. In 2025, it posted ₩3.9 trillion ($2.67 billion) in operating profit — up 172% year-over-year. Revenue hit ₩29.9 trillion ($20.5 billion), the highest in the company’s history. The stock has risen from ₩186,000 to ₩495,000 in twelve months, yet all 16 covering analysts maintain Buy ratings with an average target of ₩581,000 — implying 44% further upside from the current ₩402,000.

HD KSOE is not a single shipyard. It is the world’s largest shipbuilding conglomerate — a holding company that controls three major yards (HD Hyundai Heavy Industries, HD Hyundai Samho, HD Hyundai Mipo), the world’s largest marine engine manufacturer, and an offshore engineering division. Together, these entities can build virtually every type of vessel: LNG carriers, VLCCs, container ships, naval warships, submarines, and floating production units. No other publicly traded company on earth matches this breadth.

The timing of this analysis is deliberate. 2026 marks a critical inflection for global shipbuilding. U.S. LNG export projects are ramping up, driving an expected 115 LNG carrier orders. Simultaneously, concerns about a 14.6% decline in total global newbuilding orders are emerging. Is this the peak of the cycle — or is the structural upcycle still in its middle innings? The answer lies in the numbers, the backlog, and the unprecedented convergence of LNG demand, green fleet transition, and aging vessel replacement. For the land-based infrastructure side of this broader capex cycle, see our HD Hyundai Electric analysis.

HD Korea Shipbuilding isn’t just riding a cycle — it has fundamentally transformed its profit structure. Operating margin went from -2% to 13% in three years. The question is whether this transformation is permanent or temporary.

✔ How HD KSOE grew operating profit from a loss to $2.67B in three years

✔ The three profit engines: shipbuilding, marine engines, and offshore

✔ Why the LNG carrier super-cycle and green fleet transition are structural

✔ The vertically integrated engine business that competitors don’t have

✔ An honest assessment of cycle risk and valuation at P/E 10–12x

HD Korea Shipbuilding Financials — What the Numbers Tell Us

| Metric | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Revenue | $12.5B | $14.6B | $17.5B | $20.5B |

| Operating Income | -$247M | $436M | $980M | $2,670M |

| Operating Margin | -2.0% | 3.0% | 5.6% | 13.0% |

| Shipbuilding Revenue | — | — | $15.1B | $17.1B |

| Engine/Machinery Revenue | — | — | — | $2.93B |

| 2025 New Orders | — | — | — | $17.6B |

Source: HD KSOE filings, Korea Herald | USD conversions approximate at ₩1,460/$ | FY2025 consolidated

The standout number: operating margin swung from -2% to 13% in three years

The headline profit growth — 172% — is dramatic enough. But the margin transformation is the real story. In 2022, HD KSOE was losing money. By 2025, it was generating a 13% operating margin on $20.5B in revenue. This isn’t a cyclical bounce; it represents a fundamental shift in business quality.

Two structural drivers explain the transformation. First, the “P-MIX” (product mix) improved dramatically. Low-price vessels ordered during 2020–2022 have been delivered, and high-price LNG carriers and container ships ordered in 2023–2024 are now flowing through the income statement. Newbuilding prices are 50%+ above 2020 levels and remain elevated. A single LNG carrier contracts at $250–300M — ten times the price of a standard bulk carrier. Second, “smart yard” productivity improvements using AI-based process optimization, digital twin technology, and automated welding have reduced costs per vessel without adding headcount.

Q4 2025 was particularly striking: revenue of ₩8.15T ($5.58B) and operating profit of ₩1.04T ($712M) — the first quarter in which operating profit exceeded $700M. The quarterly run rate suggests 2026 could sustain or even exceed the 2025 annual figure.

Can these numbers sustain?

As of Q3 2025, the combined order backlog for Korea’s three major shipbuilders (HD KSOE, Hanwha Ocean, Samsung Heavy Industries) stood at approximately ₩135T ($92B) — representing 3–4 years of work. HD KSOE alone achieved $17.6B in new orders, reaching 97.4% of its $18.05B annual target. Critically, these orders were booked at elevated newbuilding prices, meaning the high-margin backlog will flow through the P&L over 2026–2028, potentially pushing operating margins even higher than the current 13%. Analysts project 2026 revenue above ₩30T with operating profit exceeding ₩4T.

The financial turnaround is clear. But for investors unfamiliar with Korean shipbuilding’s complex corporate structure, the next question is: how exactly is this conglomerate organized, and where does the profit come from?

How HD Korea Shipbuilding Makes Money — Business Model Breakdown

Think of HD KSOE as the “Berkshire Hathaway of shipbuilding” — a holding company that controls three world-class shipyards, the planet’s largest marine engine manufacturer, and an offshore engineering unit. The group can build virtually every vessel type: LNG carriers, VLCCs, container ships, bulk carriers, naval warships, submarines, and floating production units. No other publicly traded shipbuilding company matches this breadth of capability.

Pillar 1 — Shipbuilding (~84% of Revenue, $17.1B)

The shipbuilding segment generated ₩25.0T ($17.1B) in revenue and ₩3.3T ($2.27B) in operating profit in 2025 — a 120% profit increase YoY. Three yards constitute the production base. HD Hyundai Heavy Industries (HDHI) is the flagship: $12B revenue, $1.39B operating profit, operating the world’s largest single-site shipyard in Ulsan. HD Hyundai Samho contributed $5.5B revenue and $933M in operating profit. HD Hyundai Mipo, specializing in mid-size and specialized vessels, added $2.5B revenue and $246M profit.

The competitive moat in shipbuilding is the LNG cargo containment system. LNG must be transported at -163°C (-261°F), requiring extraordinarily precise insulation and containment technology (Mark III and NO96 membrane systems). Globally, only Korean shipbuilders (HD KSOE, Samsung Heavy, Hanwha Ocean) and a small number of Chinese yards possess this capability — and Korean yards command the quality premium. HD KSOE has delivered more LNG carriers than any other group in history.

The critical differentiator versus Hanwha Ocean (analyzed in our Hanwha Aerospace deep dive) is vessel-type diversification. Hanwha Ocean concentrates on LNG carriers and naval vessels. HD KSOE builds everything — LNG, VLCC, container, bulk, special-purpose, and military. This diversification provides a natural hedge: if LNG orders slow, container or tanker demand can fill the gap.

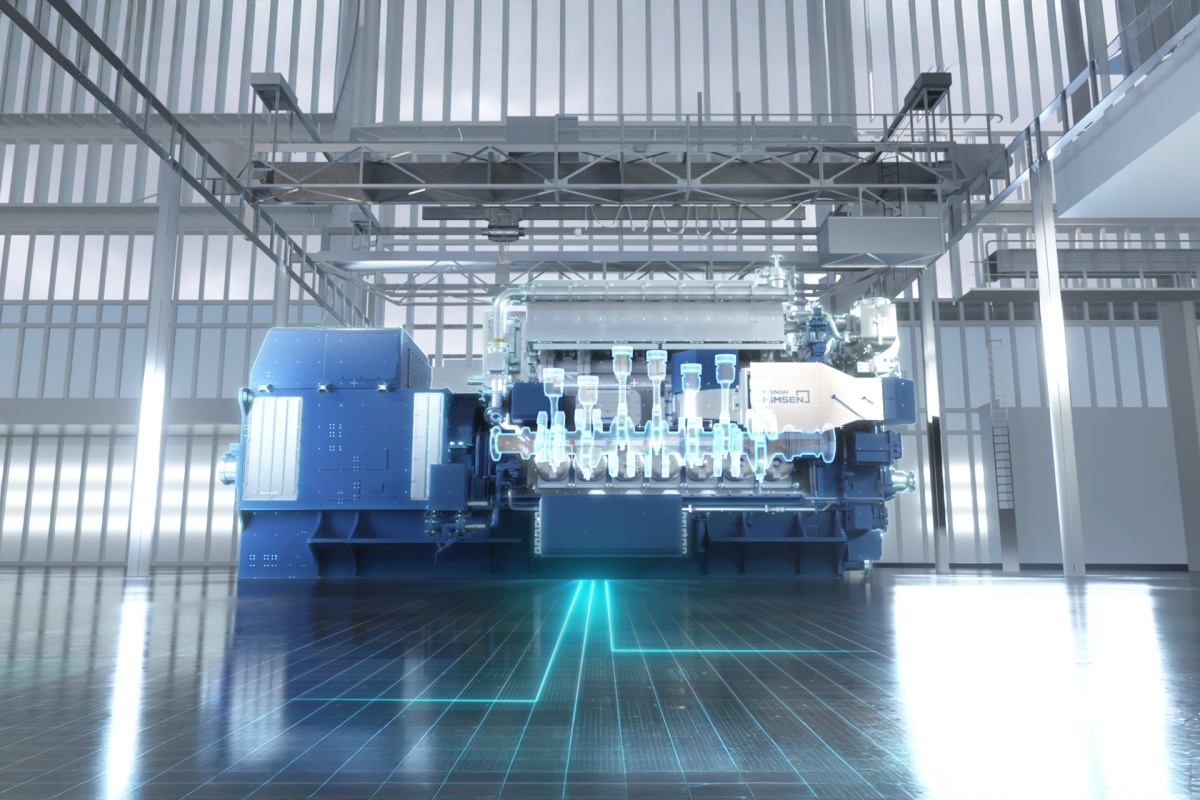

Pillar 2 — Engine & Machinery (~14% of Revenue, $2.93B)

This is HD KSOE’s secret weapon — and the single biggest structural advantage over every Korean and most global competitors. The engine/machinery segment generated ₩4.29T ($2.93B) in revenue and ₩774.6B ($530M) in operating profit in 2025, yielding an approximately 18% operating margin — higher than the shipbuilding segment’s 13%.

Marine engines are the heart of a ship. A main low-speed two-stroke engine costs tens of millions of dollars per unit. Only two companies in the world design these engines under license (MAN Energy Solutions and WinGD/Wärtsilä), and fewer than ten can actually manufacture them. HD Hyundai is the world’s largest marine engine producer by volume. As the industry transitions to eco-friendly fuels (LNG dual-fuel, methanol, ammonia), engine complexity and pricing are rising — directly benefiting HD KSOE’s margins.

The vertical integration advantage is powerful. HD KSOE installs its own engines in its own ships. Hanwha Ocean and Samsung Heavy Industries must source engines externally. This self-supply creates three advantages: lower procurement costs, internalized engine profit, and the ability to offer shipowners a “vessel + engine” package deal that competitors cannot match. The engine division alone generated $530M in operating profit in 2025 — roughly equivalent to Samsung Heavy Industries’ entire annual profit.

Pillar 3 — Offshore Engineering (~4% of Revenue, $850M)

The offshore division was Korean shipbuilding’s greatest trauma. In the 2010s, aggressive low-price bidding on offshore projects generated billions in losses across the industry. HD KSOE was not immune. But in 2025, the offshore segment finally returned to profitability: ₩1.24T ($850M) in revenue and ₩138B ($94M) in operating profit — a turnaround from losses the prior year.

The toxic legacy projects from the COVID era have been largely worked off. New contracts are being signed at appropriate margins. If oil prices remain stable, FPSO (floating production, storage, and offloading) orders could revive, adding another growth vector. However, given the traumatic history, the market applies a significant discount to offshore earnings — meaning any sustained profitability here would be viewed as incremental upside rather than a base-case expectation.

The “what if it didn’t exist” test

Transporting the world’s LNG requires vessels this company builds. Maintaining global container logistics requires vessels this company builds. The Korean Navy’s next-generation destroyers and submarines will be built by this group. HD KSOE is infrastructure — as essential to global energy logistics as pipelines are to onshore distribution.

As I covered in the Doosan Enerbility analysis, the energy value chain runs from generation to transmission to distribution to transportation. HD KSOE handles the final link: moving energy across oceans. HD Hyundai Electric builds the transformers that deliver power on land; HD KSOE builds the ships that deliver energy by sea.

With the business model understood, the next question: why is the global environment so favorable?

Why Shipbuilding Now — The Bigger Picture

Three structural megatrends are converging to create what many industry observers call a shipbuilding “super-cycle.”

Market size and growth

The Clarksons Newbuilding Price Index has risen 50%+ since late 2020. Clarkson Research projects approximately 115 LNG carrier orders in 2026, driven by U.S. LNG export terminal project FIDs (Final Investment Decisions) reaching execution phase. Container ship ordering remains robust as top-tier liner companies expand fleets and smaller operators replace aging tonnage with eco-compliant vessels. The tanker market is also inflecting: VLCC and Suezmax orderbooks are at historically elevated levels, driven by OPEC+ production increases and aging fleet replacement needs.

Regulatory and policy tailwinds

The U.S. “MASGA” (Make American Shipbuilding Great Again) initiative is pursuing technology partnerships with Korean shipbuilders to rebuild domestic naval construction capability. America’s commercial shipbuilding capacity has effectively collapsed — Korean technology and production expertise are being leveraged to support U.S. Navy fleet expansion. This opens a new market for Korean yards’ military vessel and technology export businesses.

IMO (International Maritime Organization) greenhouse gas regulations tightening from 2030 will require either retrofitting existing fleets with green propulsion or replacing them entirely with new eco-friendly vessels. This “green transition mandate” creates structural ordering demand through at least 2035, independent of the traditional shipping cycle. Ships powered by conventional fuels will face increasing operating penalties, making new eco-friendly vessels economically necessary regardless of freight rates.

Five years ago vs. today — the supply bottleneck

Five years ago, shipbuilding was considered a “sunset industry.” The 2021–2025 ordering boom changed everything. Global orderbook-to-fleet ratio reached 14.1% — well above the 10.2% ten-year average. Dock slots at major yards are booked through 2028–2029. Even if a shipowner places an order today, delivery won’t occur for 3–4 years. This capacity constraint supports pricing power and protects margins for incumbent builders with secured backlogs.

China commands ~59% of global ship orders by volume, versus Korea’s ~21%. But in high-value segments — LNG carriers, large container ships, naval vessels — Korean yards maintain technological superiority and command significant price premiums. The competitive dynamic is similar to semiconductors: China leads in commodity products (bulk carriers, standard tankers), while Korea dominates in advanced, high-margin segments.

3 Reasons to Watch HD Korea Shipbuilding

Catalyst 1 — 3–4 Year Order Backlog at Record-High Prices

The combined order backlog for Korea’s three major shipbuilders stands at approximately $92 billion — over 3 years of production capacity. HD KSOE’s 2025 new orders of $17.6B nearly met its $18.05B target.

The backlog is not just large; it is high-quality. Orders placed in 2023–2025 were contracted at newbuilding prices 50%+ above 2020 levels. As these orders convert to revenue over 2026–2028, operating margins should expand further — potentially reaching 15% by H1 2026 as the highest-priced vessels enter the delivery pipeline. This creates a paradox: the best earnings may still be ahead, even though the stock has already risen significantly.

The catalyst for backlog extension is clear: 2026 LNG carrier orders. Qatar Energy’s fleet expansion, U.S. Gulf Coast LNG terminal projects, and Mozambique/Papua New Guinea project FIDs could collectively drive 100+ LNG carrier orders, the majority of which would go to Korean yards given their technological dominance in LNG containment systems.

Catalyst 2 — Vertically Integrated Engine Business (Competitors Don’t Have This)

HD KSOE’s engine/machinery division generated $530M in operating profit at an 18% margin — a profit stream that Hanwha Ocean and Samsung Heavy Industries structurally cannot replicate.

This vertical integration means HD KSOE captures margin at two points in the value chain: once when it builds the ship, and again when it installs its own engine. Competitors must pay an external engine supplier, eroding their margin. As the global fleet transitions to dual-fuel (LNG), methanol, and ammonia propulsion, engine complexity and unit values are increasing — amplifying the profit contribution from this division. The $530M engine profit in 2025 is roughly equivalent to Samsung Heavy’s entire annual operating income — earned from a segment that HD KSOE’s direct Korean competitors simply don’t have.

Catalyst 3 — P/E 10–12x with 44% Analyst Upside — Cheapest in the Korean Infra Complex

At a trailing P/E of 10–12x, HD KSOE is by far the cheapest name in the Korean infrastructure investment universe. Hanwha Aerospace trades at 47x, HD Hyundai Electric at 40x. Yet HD KSOE’s operating profit grew 172% — faster than either of them.

The low multiple reflects the market’s ingrained skepticism about shipbuilding durability — the “cycle stock” discount. But this cycle is qualitatively different from past booms: the green fleet transition mandate is regulatory, not discretionary; LNG carrier demand is tied to energy security infrastructure, not speculation; and the supply of available dock slots is physically constrained through 2028. If the market begins to reclassify HD KSOE as a “structural growth story” rather than a “cycle stock,” the re-rating potential is significant. European defense stocks (Rheinmetall) saw P/E expand from 15x to 60x once the market accepted the structural growth thesis — the same logic could apply to shipbuilding, albeit likely to a lesser degree.

The bull case is compelling. But shipbuilding has burned investors before. Let’s examine the risks.

The Bear Case — Risks You Need to Know

Shipbuilding is one of the most cyclical industries in global equity markets. Investors who remember the 2015–2020 collapse know that today’s boom does not guarantee tomorrow’s prosperity. Intellectual honesty demands a thorough risk assessment.

| ✅ Bull Factors | ⚠️ Bear Factors |

|---|---|

| 3–4 year backlog at record-high prices | Global newbuilding orders may decline 14.6% in 2026 |

| OPM: -2% → 13%, structural quality improvement | Steel plate prices and labor costs could compress margins |

| Vertically integrated engines (competitors lack this) | Chinese yards gaining LNG capability, price competition risk |

| LNG carrier ordering boom 2026–2027 | LNG project delays could create ordering gap |

| Offshore division returned to profitability | Offshore trauma from 2010s limits market trust |

| P/E 10–12x — cheapest in Korean infra complex | Cycle stock discount may persist (re-rating not guaranteed) |

| U.S. MASGA cooperation opens defense market | U.S.-China trade tensions could reduce shipping volumes |

| Smart yard AI-based productivity gains ongoing | Skilled labor shortage constraining capacity utilization |

| Green fuel engine tech leadership (ammonia, methanol) | IMO regulation delays could slow eco-vessel ordering |

Risk 1 — Order Cycle Peak and the 2028+ Question

Korea Export-Import Bank projects 2026 global newbuilding orders declining 14.6% YoY, with Korean yards’ orders down 5.3%. After five years of elevated ordering, dock slots are saturated and shipowners may delay new commitments as newbuilding prices plateau. This doesn’t immediately affect 2026–2027 earnings (which are driven by existing backlog), but it raises a critical question: what happens to the backlog in 2028 and beyond? If 2026–2027 new orders fall significantly, the backlog could erode, creating earnings risk from 2029 onward. This is the fundamental cycle risk of shipbuilding investment.

However, the LNG carrier pipeline provides a structural buffer. With 115+ LNG carriers projected for 2026 orders alone, and IMO green regulations mandating fleet renewal through 2035, the ordering trough — when it comes — should be shallower than in past cycles.

Risk 2 — Cost Pressures and Chinese Competition

Steel plate (the primary raw material for hull construction) prices and labor costs are the key margin variables. Korean shipbuilding faces a chronic shortage of skilled workers after the 2010s restructuring drove experienced welders and fitters out of the industry. Subcontractor costs are rising steadily. If steel prices spike simultaneously, the margin expansion narrative could stall.

Chinese shipbuilders are the elephant in the room. CSSC (China State Shipbuilding Corporation) already commands ~59% of global orders by volume and is actively developing LNG containment technology. While Korean yards maintain a significant quality gap in LNG carriers today, that gap is narrowing. If China achieves LNG carrier capability at scale with lower pricing, it would create downward pressure on newbuilding prices — directly threatening HD KSOE’s margin premium.

Despite these risks

The critical point is that P/E 10–12x already prices in substantial cycle risk. The market is not treating HD KSOE as a growth stock — it is applying a deep cyclical discount. If the structural thesis (LNG transition + green fleet + engine vertical integration) is even partially correct, the current multiple leaves significant room for re-rating. At the same time, the 3–4 year backlog provides a concrete earnings floor that limits downside even in a weaker ordering environment.

My Take — Here’s How I See HD Korea Shipbuilding

Of the three companies analyzed in this series — Hanwha Aerospace (defense), HD Hyundai Electric (power infrastructure), and HD Korea Shipbuilding (shipbuilding) — HD KSOE has the lowest valuation and the highest analyst-implied upside. Hanwha Aerospace trades at P/E 47x, HD Hyundai Electric at 40x, and HD KSOE at 10–12x. Yet HD KSOE’s operating profit grew 172% — the fastest of the three.

P/E 10x with 172% operating profit growth. This is either the market correctly pricing cycle risk — or a mispricing waiting to be corrected. The answer depends on whether the LNG transition and green fleet mandate are cyclical or structural.

Bull scenario

H1 2026 P-MIX improvement pushes operating margin to 15%. Large-scale 2026 LNG orders confirm the structural demand thesis. The market begins to reclassify HD KSOE from “cycle stock” to “structural growth” — P/E expands toward 15–18x. Target price of ₩640,000 ($438) is achievable. If K-submarine projects materialize, a defense premium adds further upside.

Bear scenario

Global ordering declines sharply, Chinese yards capture meaningful LNG market share, and steel/labor costs squeeze margins below 10%. The market maintains or deepens its cyclical discount. Stock price ranges sideways in the ₩350,000–400,000 band rather than declining sharply, given the backlog floor — but the re-rating thesis fails to materialize.

At the current ₩402,000 ($275), the stock is trading at roughly 30% below the ₩581,000 analyst consensus target. For investors building a “Korean infrastructure basket” — combining defense (Hanwha Aerospace), power equipment (HD Hyundai Electric), and shipbuilding (HD KSOE) — this is the cheapest entry point in the basket and the one with the highest consensus upside.

HD Korea Shipbuilding FAQ

Q. What is HD Korea Shipbuilding’s corporate structure?

HD KSOE is the intermediate holding company for HD Hyundai Group’s shipbuilding operations. It controls three shipyards: HD Hyundai Heavy Industries (large vessels, Ulsan), HD Hyundai Samho (mid-size, Yeongam), and HD Hyundai Mipo (small/specialized, Ulsan). It also houses the marine engine division and offshore engineering. Buying HD KSOE stock gives exposure to all three yards’ consolidated results. HD Hyundai Heavy Industries is also separately listed for investors wanting pure exposure to the flagship yard.

Q. How does HD KSOE compare to Hanwha Ocean?

HD KSOE is roughly 3x larger: $20.5B revenue and $2.67B operating profit versus Hanwha Ocean’s $8.7B and $760M. HD KSOE builds all vessel types while Hanwha Ocean focuses on LNG carriers and naval vessels. The most critical difference is engine manufacturing: HD KSOE produces its own marine engines (generating $530M in profit), while Hanwha Ocean must source engines externally. HD KSOE’s diversification provides natural hedging against individual segment downturns.

Q. Can global investors buy HD KSOE stock?

HD KSOE trades on the Korea Exchange (KOSPI) under ticker 009540. It is accessible through international brokerages offering Korean equity trading. No ADR listing exists. The stock is KRW-denominated, exposing foreign investors to USD/KRW currency risk. The current exchange rate of ~₩1,460–1,510/$ is favorable for Korean exporters. HD Hyundai Heavy Industries (329180.KS), the flagship subsidiary, is also separately listed and offers more concentrated exposure to the core shipbuilding business.

Q. Why is the P/E so low despite strong growth?

Shipbuilding is traditionally classified as a deep cyclical industry. The market applies a structural discount because past boom-bust cycles (most recently 2010–2020) demonstrated that high profits can evaporate rapidly. The P/E of 10–12x reflects the market’s assumption that current margins are unsustainable long-term. However, bulls argue this cycle is structurally different: green fleet mandates, LNG energy transition, and physical capacity constraints provide a floor that past cycles lacked. Resolution of this debate would be the catalyst for re-rating.

The Bottom Line — 3 Things to Remember

One. HD Korea Shipbuilding posted record $20.5B revenue and $2.67B operating profit in 2025, with operating margin transforming from -2% to 13% in three years. This is not a simple cyclical rebound — it reflects high-value vessel mix improvement, smart yard productivity gains, and a structural shift toward eco-friendly ship demand. With 3–4 years of backlog at elevated prices, the best earnings quarters may still be ahead as 2023–2025 high-price orders flow through the P&L.

Two. The vertically integrated engine business is HD KSOE’s most powerful competitive moat. Generating $530M in operating profit at 18% margins, this division provides a profit stream that direct competitors structurally cannot replicate. Combined with the industry’s broadest vessel-type portfolio and three world-class shipyards, HD KSOE occupies a position in global shipbuilding that has no true peer.

Three. The risk is cycle timing. Global ordering may moderate in 2026, Chinese yards are building LNG capability, and input costs are rising. But P/E 10–12x already prices in substantial cycle risk. The 44% gap to analyst consensus targets suggests the market may be underweighting the structural case. For investors building a Korean infrastructure portfolio — defense, power equipment, and shipbuilding — HD KSOE is the cheapest entry point and the one with the most consensus upside remaining.

Energy generation (Doosan Enerbility), power delivery (HD Hyundai Electric), and energy transportation (HD Korea Shipbuilding) — together, these three companies form the complete energy infrastructure value chain. HD KSOE is the final piece of the puzzle, and at P/E 10x, it’s the cheapest piece to acquire.

If you found this analysis useful, consider sharing it with fellow investors who follow shipbuilding and energy infrastructure themes.

Next up, I’ll be analyzing Hyundai Rotem — the dual-engine company running on K2 tanks and KTX high-speed rail. A different flavor of Korean defense and industrial investment.

This article is based on data as of April 2026. Updated after quarterly earnings (May 2026 expected).

Disclaimer: This article reflects the author’s personal research and analysis for informational purposes only. It is not a recommendation to buy or sell any security. Investment decisions and their consequences are the reader’s responsibility. Always verify with the latest filings and consult a qualified financial advisor.

Related Reading

- Hanwha Aerospace: $18B Revenue, $25B Backlog, and the Rise of a Global Defense Platform

- HD Hyundai Electric: 27.6% Margin, $6.7B Backlog — The AI Power Play

- Hyosung Heavy Industries: The Hidden Champion of AI Power Infrastructure

- Doosan Enerbility: The Nuclear Renaissance Play

- SK Hynix Deep Dive: How HBM Is Reshaping the Memory Industry