KEPCO KPS Analysis — Korea’s Nuclear Maintenance Monopoly

This KEPCO KPS analysis examines the only company in South Korea with an exclusive mandate to maintain every nuclear reactor in the country — 26 operating units, 2 permanently shut down, and 2 more in commissioning. In 2024, KEPCO KPS posted record revenue of ₩1.56 trillion ($1.1 billion), record operating income of ₩210 billion, and an operating margin north of 13%. The stock trades at roughly 10x earnings with a dividend yield above 4%. For a government-backed monopoly riding a global nuclear renaissance, those numbers deserve a closer look.

If you’ve been watching the Korean nuclear energy export story unfold — the $18.6 billion Czech Dukovany deal, the Romania Cernavoda refurbishment, the talk of U.S. market entry — KEPCO KPS is the company that shows up after the reactors are built. It’s the maintenance arm. And in the nuclear business, maintenance is where the long-term, recurring revenue lives.

The timing is worth noting. South Korea just signed its landmark Czech nuclear contract in mid-2025, and KEPCO KPS is the designated commissioning and maintenance partner for Team Korea. Domestically, multiple aging reactors are approaching life-extension decisions that could unlock ₩200 billion or more in annual maintenance revenue per unit. Meanwhile, Q3 2025 showed a sharp recovery — revenue up 11%, operating profit up 13% — after a seasonally weak first half.

KEPCO KPS is a rare asset: a publicly traded monopoly in nuclear maintenance, backed by the Korean government, with a multi-decade growth runway in global nuclear exports.

✔ KEPCO KPS’s record-breaking 2024 financials — and why 2025 had a rocky start

✔ How the business model works across nuclear, thermal, and overseas segments

✔ Why the global nuclear renaissance matters more for this stock than any reactor builder

✔ Three catalysts — Czech exports, domestic life extensions, Romania revenue

✔ The bear case, an honest valuation take, and how global investors can access this stock

KEPCO KPS Financials — What the Numbers Tell Us

| Metric | 2022 | 2023 | 2024 | 2025E |

|---|---|---|---|---|

| Revenue | $1.03B (₩1.43T) | $1.11B (₩1.53T) | $1.13B (₩1.56T) | $1.19B (₩1.64T) |

| Operating Income | $95M (₩131B) | $144M (₩199B) | $152M (₩210B) | $165M (₩228B) |

| Operating Margin | 9.2% | 13.0% | 13.5% | 13.9% |

| Net Income | $72M (₩100B) | $118M (₩163B) | $125M (₩172B) | $143M (₩197B) |

| P/E Ratio | 14.9x | 9.4x | 11.0x | 10.3x |

| EV/EBITDA | 8.2x | 5.8x | 6.0x | 5.7x |

| Dividend Yield | 3.9% | 6.3% | 5.3% | 4.9% |

Source: KEPCO KPS DART filings, Mirae Asset Securities | USD conversions approximate at ₩1,380/$ | K-IFRS consolidated

The standout number: operating margin climbing from 9.2% to 13.5% in just two years

This isn’t a company that grew by adding headcount. KEPCO KPS improved labor productivity by 6.8% year-over-year in 2024, hitting a record ₩165 million per employee. The company cut ₩56.9 billion in discretionary spending through a dedicated cost control task force launched in mid-2024. Revenue grew modestly at 1.5%, but profitability expanded significantly because the revenue mix shifted toward higher-margin nuclear maintenance work.

Year-over-year, the nuclear/pumped storage segment — now 38.7% of revenue — grew meaningfully as new units like Shin-Hanul 2 entered regular maintenance cycles. Thermal maintenance held steady despite competitive pressures from private contractors. The overseas segment contributed 11.8% of revenue, with projects spanning from UAE to South Africa to Indonesia.

But 2025 started rough. Q1 2025 revenue dropped 16% year-over-year to ₩288 billion, and operating income collapsed 85% to just ₩7.8 billion. The cause? Fewer scheduled nuclear outages in Q1 — maintenance revenue is inherently lumpy, concentrated in quarters when reactors go offline for planned maintenance. By Q3 2025, the company roared back with 11% revenue growth and 13% operating profit growth. This seasonality is structural, not a red flag.

Can these numbers sustain?

Consensus estimates from Mirae Asset and KB Securities project 2025 revenue of ₩1.64 trillion and 2026 revenue of ₩1.79 trillion — implying 5-9% annual growth. The growth driver is clear: more nuclear reactors entering maintenance cycles domestically, plus Romania Cernavoda revenue recognition starting in late 2025 or early 2026. The company’s own value enhancement plan targets ₩1.9 trillion in revenue by 2028.

The financials tell one story — steady, profitable, well-managed. But the real question is whether the business model can scale beyond Korea. That’s where it gets interesting.

How KEPCO KPS Makes Money — Business Model Breakdown

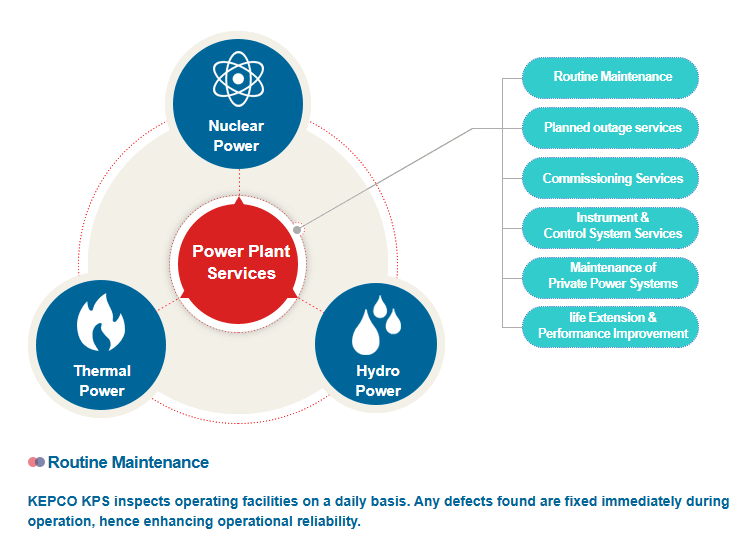

KEPCO KPS is conceptually simple: it maintains power plants. But the simplicity is deceptive. This is a company with 77 operational sites across Korea, monopoly positions in nuclear maintenance, and a growing overseas footprint. Think of it as the Rolls-Royce of Korean power infrastructure — not the car maker, but the jet engine company that earns most of its revenue from long-term service contracts rather than one-time equipment sales.

Pillar 1 — Nuclear & Pumped Storage Maintenance (~39% of Revenue)

This is the crown jewel. KEPCO KPS is the sole entity authorized to perform routine and planned preventive maintenance on all 26 operating nuclear reactors in South Korea, operated by Korea Hydro & Nuclear Power (KHNP). No private contractor can legally compete for this work — it’s a regulatory monopoly rooted in safety requirements and decades of accumulated expertise.

The revenue model is straightforward: each reactor goes offline periodically for scheduled maintenance (planned outages), during which KEPCO KPS performs turbine inspections, generator overhauls, steam generator eddy current testing, and safety system checks. Each operating reactor generates roughly ₩20 billion or more in annual maintenance revenue. With new reactors like Shin-Hanul 2 (2024) and Saeul 3 and 4 (2025-2026) entering service, the addressable domestic nuclear fleet is expanding.

The profitability here is structurally high because nuclear maintenance requires specialized certifications, proprietary diagnostic tools (AI-based fault diagnosis, 3D printing for discontinued parts), and institutional knowledge that simply cannot be replicated by new entrants. KEPCO KPS has been doing this since Korea’s first reactor — Kori Unit 1 — went commercial in 1978.

Where this pillar gets exciting is the broader Korean nuclear export push, which I’ve covered in the context of reactor builders. KEPCO KPS isn’t building reactors — it’s the company that keeps them running for 60+ years after construction ends.

Pillar 2 — Thermal Power Plant Maintenance (~35% of Revenue)

KEPCO KPS maintains coal, LNG, and combined-cycle power plants operated by Korea’s five major generation subsidiaries (Korea South-East Power, Korea Southern Power, Korea East-West Power, Korea Western Power, and Korea Midland Power). Unlike nuclear, this market is partially open to competition — the Korean government introduced competitive bidding for thermal maintenance in stages, and KEPCO KPS’s market share has gradually declined from around 50% to roughly 47%.

Still, the company retains dominant share because of its institutional relationships, technical depth, and track record. Thermal maintenance is bread-and-butter work: turbine overhauls, boiler inspections, electrical system maintenance. The margins are lower than nuclear, and the long-term outlook is mixed — Korea plans to retire older coal plants and replace them with LNG and zero-carbon sources. But new combined-cycle plants (like the Daegu and Cheongju cogeneration facilities that KEPCO KPS won in 2024) keep the segment alive.

The strategic question for investors: will the decline in coal maintenance revenue be offset by growth in nuclear and overseas? The consensus answer is yes, but the transition creates quarterly volatility — exactly what spooked investors in Q1 2025 when thermal outage schedules shifted.

Pillar 3 — Overseas & External Projects (~20% of Revenue)

This is the growth engine. KEPCO KPS has operated internationally since 1982, with a presence in over 25 countries — India, Pakistan, Uruguay, Jordan, South Africa, UAE, Indonesia, and now Europe. The overseas backlog stood at ₩1.2 trillion as of mid-2025, a number that’s set to grow significantly with the Romania Cernavoda contract (₩2.8 trillion total project value) and the Czech Dukovany project where KEPCO KPS handles commissioning and long-term maintenance.

The external segment (non-KEPCO group clients) includes maintenance work for Korea District Heating Corporation, private power producers, and industrial clients like POSCO. It’s a diversification play — reducing dependence on the KEPCO group, which currently accounts for over 80% of consolidated revenue.

In February 2026, KEPCO KPS signed a collaboration agreement with Spain’s GDES to expand into the French and Spanish nuclear maintenance markets, as reported by the American Nuclear Society. This is significant because it represents independent overseas expansion, separate from the Team Korea consortium model. If KEPCO KPS can establish itself as a credible nuclear maintenance provider in European markets, the revenue potential dwarfs anything the company has achieved domestically.

The “what if it didn’t exist” test

If KEPCO KPS disappeared tomorrow, every nuclear reactor in South Korea would need to find a new maintenance provider. There isn’t one. No private Korean company has the certifications, the trained workforce, or the decades of reactor-specific knowledge to step in. The company is, quite literally, irreplaceable for Korea’s nuclear fleet. That’s the definition of a moat.

I covered this broader nuclear value chain dynamic in the HD Hyundai Electric analysis, which examines the transmission and distribution side of Korea’s power infrastructure.

So far we’ve established the monopoly. But monopolies in shrinking markets don’t make good investments. The question is whether the market is growing — and the answer requires looking at the bigger picture.

Why Nuclear Energy Now — The Bigger Picture

Three years ago, nuclear energy was a political liability. Post-Fukushima sentiment had driven phase-out policies across East Asia and Europe. Today, nuclear is experiencing arguably its strongest political tailwind since the 1970s oil crisis. What changed?

The global policy reversal

In the United States, President Trump signed executive orders to quadruple nuclear capacity from 100GW to 400GW, streamline NRC approval processes, and actively court Korean reactor builders. The U.S. Department of Energy has signaled interest in Korean APR-1400 technology. In Europe, the Czech Republic signed an $18.6 billion contract with Korea’s Team Korea consortium for two new reactors at Dukovany — the first major European nuclear contract awarded to a Korean consortium. France, once the sole European nuclear champion, has welcomed Korean maintenance expertise through the KEPCO KPS-GDES partnership. Romania’s Cernavoda refurbishment adds another European foothold.

In Asia, India and Pakistan have existing relationships with KEPCO KPS, while Kazakhstan is pursuing aging plant performance improvements. Turkey has signed an MOU with KEPCO for nuclear cooperation. The global pipeline of nuclear maintenance opportunities has never been this large.

Market size and growth

The global nuclear power plant maintenance market was valued at approximately $45 billion in 2024 and is projected to grow at 4-6% CAGR through 2035, driven by life extensions of aging fleets (particularly in the U.S. and Europe) and new builds in Asia and the Middle East. KEPCO KPS currently captures roughly 2.5% of this global market — almost entirely from Korea. Even a modest increase in overseas market share would meaningfully move the needle on a ₩1.5 trillion revenue base.

Domestic tailwinds: Korea’s 11th Basic Electricity Plan

South Korea’s latest power supply plan calls for two additional nuclear reactors by 2038, plus life extensions for aging units. Kori Units 2-4 have already reached their design life and are offline; decisions on whether to extend them could unlock ₩200+ billion in annual maintenance revenue per unit for KEPCO KPS. The company’s entire domestic nuclear revenue today is around ₩650 billion — adding even two or three life-extended units would represent meaningful growth without any overseas expansion at all.

I explored how this power infrastructure buildout connects to the broader Korean industrial value chain in the HD Korea Shipbuilding analysis.

The macro setup is clear: nuclear is back, Korea is exporting it, and KEPCO KPS is the maintenance monopoly. But what specifically will drive the stock from here? That brings us to the investment thesis.

KEPCO KPS Analysis — 3 Reasons to Watch This Stock

Catalyst 1 — Czech & Romania Contracts Create a Decade of Overseas Revenue

KEPCO KPS’s overseas revenue is set to roughly double from ₩178 billion (2024) to ₩269 billion (2026E), with further acceleration beyond.

The Romania Cernavoda pressure tube replacement and facility improvement project has a total value of ₩2.8 trillion over 5-6 years. Mirae Asset estimates KEPCO KPS will recognize ₩50-100 billion annually from this project, with revenue recognition potentially starting as early as late 2025. This single contract could add 3-6% to total company revenue on an ongoing basis.

The Czech Dukovany project is even larger in scope — $18.6 billion total for two APR-1400 reactors. KEPCO KPS’s role covers commissioning (pre-commercial testing) and long-term maintenance. Based on the UAE Barakah precedent, where KEPCO KPS won the maintenance contract in 2009 but didn’t recognize revenue until 2015, the Czech revenue will likely start around 2033-2035 when the first reactor reaches commissioning. But the contract backlog creates visibility today and supports a higher valuation multiple.

Beyond Romania and Czech Republic, KEPCO KPS has been pursuing maintenance contracts in Kazakhstan (aging plant performance improvements), Uruguay, and now Spain/France through the GDES partnership. The total addressable overseas pipeline has grown from essentially zero meaningful contracts five years ago to multiple billions of won in secured and probable backlog.

Catalyst 2 — Domestic Nuclear Life Extensions Are a Revenue Multiplier

Each reactor life extension adds an estimated ₩200+ billion in cumulative maintenance revenue over the extended operating period — and multiple units are approaching decision points.

Korea currently has three reactors (Kori Units 2, 3, and 4) that have reached their design life and are offline. An additional four units will reach design life by 2028. The political and economic case for life extension is overwhelming: building new reactors costs $6-10 billion each and takes a decade; extending existing ones costs a fraction and delivers baseload power within 2-3 years of refurbishment.

For KEPCO KPS, a life-extension project is the best possible business outcome. It requires comprehensive safety inspections, equipment replacements, system upgrades, and years of follow-on maintenance — all performed exclusively by KEPCO KPS. Kiwoom Securities estimates each life-extended unit generates approximately ₩200 billion or more in cumulative maintenance revenue. With seven units potentially eligible for extension over the next five years, this represents a domestic growth opportunity that rivals the overseas expansion in absolute terms.

The 11th Basic Electricity Plan’s endorsement of nuclear expansion provides the political cover needed for these decisions. If even half of the eligible units receive life extensions, KEPCO KPS’s nuclear revenue segment could grow by 20-30% from current levels on domestic activity alone.

Catalyst 3 — Shifting Revenue Mix Toward Higher-Margin Nuclear Work

As nuclear’s share of revenue grows and lower-margin thermal work shrinks, blended margins should structurally improve — even without pricing power.

In 2022, nuclear/pumped storage accounted for about 35% of revenue with thermal at roughly 40%. By 2024, nuclear had overtaken thermal as the largest segment at 38.7%. Mirae Asset projects nuclear to reach 41-42% of revenue by 2026, while thermal declines to around 32%. This mix shift is the primary driver behind the margin expansion from 9.2% (2022) to a projected 13.7% (2026E).

Nuclear maintenance commands higher margins because: the work is non-competitive (monopoly pricing), the technical complexity requires specialized labor (high barriers), and the cost of failure is catastrophic (nuclear safety premium). By contrast, thermal maintenance faces competitive bidding and price pressure from private contractors.

The beauty of this dynamic is that it works even if KEPCO KPS does nothing new. As Korea’s energy mix naturally shifts toward nuclear and away from coal — a process already underway through government policy — the company’s revenue mix improves automatically. Any incremental overseas nuclear revenue simply accelerates the trend.

Bonus — SMR (Small Modular Reactor) Optionality

KEPCO KPS has signed cooperation agreements with KHNP and Daewoo E&C for SMR development, and is collaborating with the Korea Atomic Energy Research Institute on high-temperature gas-cooled reactor (HTGR) projects through 2027. SMR maintenance would be a natural extension of the company’s existing capabilities. This is not in any analyst’s revenue model yet — it’s pure optionality, but optionality with a credible path to commercialization.

I covered how Korea’s tech infrastructure plays like SK Hynix benefit from similar structural tailwinds — once you’re the dominant domestic player, global expansion becomes an earnings multiplier rather than a gamble.

The bullish catalysts are clear. But every investment has a dark side. What could go wrong?

The Bear Case — Risks You Need to Know

KEPCO KPS looks like a textbook quality monopoly. But even monopolies face risks — and some of them are specific to this company’s unusual position as a government-controlled maintenance provider.

| ✅ Bull Factors | ⚠️ Bear Factors |

|---|---|

| Nuclear maintenance monopoly in Korea | Revenue heavily dependent on KEPCO group (80%+) |

| Record revenue and profitability in 2024 | Severe quarterly seasonality (Q1 consistently weak) |

| Czech + Romania overseas contracts secured | Czech revenue won’t materialize until ~2033 |

| Domestic nuclear life extensions imminent | Life extension decisions are political, not commercial |

| Revenue mix shifting to higher-margin nuclear | Thermal maintenance declining due to coal phase-out |

| 4-5% dividend yield with ~50% payout ratio | Government-controlled entity limits shareholder activism |

| AI/robotics improving labor productivity | Labor costs are largely fixed (public sector wages) |

| Westinghouse IP dispute resolved for exports | KHNP restricted from EU/US bids (Westinghouse deal limits) |

Risk 1 — Government Control and KEPCO Dependency

KEPCO (Korea Electric Power Corporation) owns 51% of KEPCO KPS, and the company is classified as a quasi-market public enterprise. This means executive appointments, wage policies, capital allocation, and dividend decisions are all influenced by government priorities — which may not always align with minority shareholder interests.

More practically, over 80% of KEPCO KPS’s revenue comes from KEPCO group companies. If KEPCO’s own financial health deteriorates (KEPCO has been running massive deficits due to electricity price caps), there could be downstream pressure on maintenance spending or payment timing. While KEPCO’s financials have been improving as the government gradually raises electricity tariffs, the structural dependency on a single loss-making parent company is a legitimate concern.

The probability of this materially impacting KEPCO KPS is moderate. Nuclear maintenance spending is non-discretionary — you can’t defer reactor safety inspections to save money. But thermal maintenance budgets have more flexibility, and the competitive bidding for thermal work means KEPCO subsidiaries can and do squeeze maintenance costs.

Risk 2 — The Long Wait for Overseas Revenue Materialization

The market is excited about Team Korea’s nuclear export wins. But investors need to understand KEPCO KPS’s position in the project timeline: it comes last. Reactor builders like Doosan Enerbility and KEPCO E&C recognize revenue during the construction phase (5-7 years). KEPCO KPS recognizes revenue during commissioning (pre-commercial testing) and then ongoing maintenance (decades). The UAE Barakah contract was won in 2009; KEPCO KPS didn’t see revenue until 2015.

For the Czech Dukovany project, construction is expected to start in 2029 with the first reactor completed by 2036. KEPCO KPS’s commissioning revenue would begin around 2033-2035 at the earliest. That’s a 7-9 year wait from today. The Romania Cernavoda project is closer (revenue expected from late 2025), but investors buying KEPCO KPS today for the Czech story need patience measured in years, not quarters.

The probability of the Czech project being delayed or restructured is low but non-zero. Anti-trust reviews briefly delayed the signing in late 2024, and the Westinghouse IP settlement included restrictions on KHNP bidding for additional EU or North American projects — limiting the growth of Team Korea’s export pipeline beyond Czech Republic.

Despite these risks

The core investment case doesn’t rely on overseas revenue alone. Domestic nuclear maintenance is growing organically through new reactor commissioning and potential life extensions. The company’s monopoly position is legally protected. And even if overseas expansion takes longer than expected, the current valuation (10-11x P/E, 4-5% dividend yield) doesn’t appear to price in much growth at all — suggesting limited downside if the bull case takes time to play out.

So what’s the honest assessment? Here’s my take.

My Take — Here’s How I See KEPCO KPS

KEPCO KPS is one of those rare stocks where the moat is almost absurdly obvious. It’s a legally protected monopoly in a growing market, trading at a utility-like multiple, with a nuclear export growth story that hasn’t been priced in yet. The dividend alone provides a 4-5% annual return while you wait for catalysts to materialize.

KEPCO KPS is a 10x P/E monopoly in the world’s most politically favored energy sector. The question isn’t whether to watch it — it’s when to size up.

Bull scenario

If Romania Cernavoda revenue starts flowing in 2026, domestic nuclear life extensions for Kori units are approved, and the Spain/France partnership gains traction, KEPCO KPS could reach ₩1.9-2.0 trillion in revenue by 2028. At 13-14% operating margins, that’s ₩260-280 billion in operating income — roughly 25-30% above current levels. A re-rating to 13-14x P/E (modest premium to current levels) would imply 40-50% upside from current prices.

Bear scenario

If nuclear life extensions stall due to political opposition, Romania revenue is delayed, and thermal maintenance continues declining faster than nuclear grows, the stock could trade sideways at 9-10x P/E. But even in this scenario, the 4-5% dividend yield provides a floor, and the nuclear monopoly ensures the business doesn’t deteriorate. The downside case is more “dead money” than “permanent capital loss.”

What entry point makes sense? The stock has rallied from ₩33,000 (April 2024 low) to around ₩62,000 — nearly doubling. A pullback to the ₩50,000-55,000 range (roughly 11-12x trailing earnings) would offer a more attractive risk-reward entry for new positions. But for long-term holders, the structural thesis doesn’t require perfect timing.

Here’s something worth thinking about: if you believe nuclear energy is entering a multi-decade renaissance, would you rather own the companies that build reactors (one-time revenue) or the company that maintains them forever (recurring revenue)?

KEPCO KPS FAQ

Q. What does KEPCO KPS actually do?

KEPCO KPS (Korea Electric Power Corporation Plant Service & Engineering, ticker 051600) is South Korea’s dominant power plant maintenance company. It performs routine maintenance, planned preventive maintenance, retrofit upgrades, and commissioning for nuclear, thermal, and renewable power plants. The company maintains all 26 operating nuclear reactors in Korea and has a growing overseas presence in 25+ countries.

Q. Can global investors buy KEPCO KPS stock?

Yes. KEPCO KPS trades on the Korea Exchange (KRX) under ticker 051600. International investors can access it through brokerages that offer KRX trading, such as Interactive Brokers, Saxo Bank, or Korean securities firms with English-language platforms. There are no ADRs available. Foreign ownership currently stands at approximately 12% of outstanding shares, and there are no foreign ownership restrictions on this stock.

Q. How is KEPCO KPS different from KEPCO (Korea Electric Power)?

KEPCO is the parent company — Korea’s national electric utility that generates, transmits, and distributes electricity. KEPCO KPS is a subsidiary focused exclusively on maintenance and engineering services. KEPCO owns 51% of KEPCO KPS. The key difference for investors: KEPCO has been running large deficits due to regulated electricity prices, while KEPCO KPS has been consistently profitable with growing margins.

Q. How exposed is KEPCO KPS to the Czech nuclear deal?

KEPCO KPS is the designated commissioning and maintenance partner for the Czech Dukovany project. However, its revenue will not begin until the reactors approach completion — likely 2033-2035. The closer-term revenue catalyst is the Romania Cernavoda refurbishment project, which is expected to generate ₩50-100 billion annually starting in late 2025 or 2026. The Czech contract is better understood as a long-term visibility event than a near-term earnings driver.

Q. Is the dividend sustainable?

KEPCO KPS has maintained a payout ratio of approximately 50% and offers a dividend yield of 4-5% at current prices. With record operating cash flows and a strong balance sheet, the dividend appears well-supported. As a quasi-public enterprise, the company faces some pressure to maintain dividends for fiscal policy reasons, which paradoxically provides additional dividend stability compared to purely private companies.

The Bottom Line — 3 Things to Remember

One. KEPCO KPS is Korea’s only nuclear power plant maintenance provider — a legal monopoly that maintains all 26 operating reactors. This isn’t a competitive advantage that can be disrupted by technology or undercut by a cheaper rival. It’s a structural moat protected by regulation, safety requirements, and nearly five decades of accumulated expertise.

Two. The growth story has two legs: overseas (Romania Cernavoda revenue starting 2025-2026, Czech Dukovany from ~2033, European market entry via GDES) and domestic (nuclear life extensions for 3-7 aging reactors, new reactor commissioning). Together, these could push revenue from ₩1.56 trillion today to ₩1.9-2.0 trillion by 2028, with margins expanding as the revenue mix tilts further toward nuclear.

Three. At 10-11x P/E with a 4-5% dividend yield, the stock is valued like a low-growth utility — but it has the growth profile of a specialty services company riding the biggest nuclear build cycle since the 1970s. The disconnect between valuation and growth potential is the opportunity.

KEPCO KPS is what happens when a regulated monopoly meets a generational growth cycle. The market is pricing the monopoly. It hasn’t fully priced the growth.

If you found this analysis useful, consider sharing it with fellow investors who follow nuclear energy and Korean infrastructure stocks.

Next up, I’ll be analyzing Korea Electric Power Corporation (KEPCO) — the parent company that controls Korea’s entire electricity grid and is attempting the most dramatic financial turnaround in Korean utility history.

This article is based on data as of April 2026. Updated after quarterly earnings.

Disclaimer: This article reflects the author’s personal research and analysis for informational purposes only. It is not a recommendation to buy or sell any security. Investment decisions and their consequences are the reader’s responsibility. Always verify with the latest filings and consult a qualified financial advisor.